Major Short Squeeze Potential On ALEC; AUUD And CUEN Continue ALF-Like Squeeze

Notice the stark difference. Just like ALF, volume tapered off significantly from the first day of the pump. But unlike ALF, BSQR continues to decline every day. It lost over 50% from $8.04 to $3.98 in that time.

BSQR is actually the normal price action while ALF is the exception. When stocks spike on heavy volume on news, then that volume dissipates, the stock price almost always trends down too. Day traders and other flippers are losing interest while the news isn't enough to attract real investors, so the price sinks. Shorts then benefit by pounding the stock downwards even further to fill stop losses, leading to the downward spiral you see on BSQR and many other stocks.

Contrast that to ALF. It went up on lower volume. Day traders were leaving the pump, but they were being replaced by long term investors who liked the news. Shorts failed to push the stock downward, so by the sixth day they were in big trouble as the stock spiked. Day traders and flippers saw the strength in ALF's stock and decided to pile in even more aggressively than before. End result? The stock price raced to $16.29 on day six and $20 a few days later.

Now let's look at AUUD's price history:

While AUUD started gaining momentum a couple of days before, we consider its breakout over $5 on June 28 to be its "day one" as it's the most similar to ALF's break out over $5 on June 15. Volume was 37 million that day and 64 million the next, but has since tapered off significantly to only 6 million on July 2. Despite that, the stock price has risen from $5.89 to $7.42, a 26% gain that is even superior to ALF. The action from June 29 to June 30 where the stock price dropped 20% and volume dropped over 90% looked very BSQR-like, until things reversed course the next two days. This reversal of the pump and dump chart is extremely significant and bullish.

AUUD is in a similar spot to ALF where shorts are starting to sweat as their attempt to push down the price failed. Day traders will soon recognize the strength in the chart and start to pile in again. Finally, news is expected as the company released its flagship Auddia app in the Appstore this past week, sparking the increase in the first place. The Android version is expected to be released while the marketing of the national launch of Auddia over the air will begin on July 5.

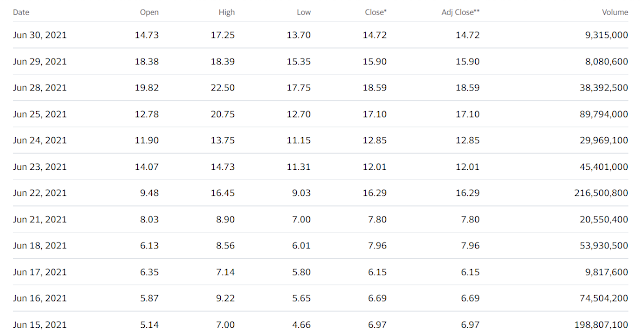

Now let's look at CUEN's price history:

CUEN's volume has dropped from 210 million down to 26 million then down to 6 million in the two days following its big pump. Despite that, the stock price has remained steady, up 4% from $6.22 to $6.45. The price performance isn't quite as compelling as AUUD, but it's already miles better than BSQR, especially considering the massive drop off in day trading volume.

The other huge bullish tell on both AUUD and CUEN is the warrants, AUUDW and CUENW respectively. This is what we said on ALF on June 20th:

"ALF is up 19% in those three days, and has nearly tripled from its May 4 close of $2.90. Its trading has been very solid since it announced the installation of 10,000 digital screens in Uber and Lyft vehicles in Miami on the 15th. While many stocks in similar situations exhibit a "pump and dump" chart and sell off days after the news, ALF has had bullish action since then. The shorts and hedge funds tried bringing it down with weak opens on June 16 and June 17. But it has failed. We mentioned above about how the warrants traded below their intrinsic value last Wednesday when it blasted off to over $9. It happened again on Friday. The $7.96 close on the stock implies an intrinsic value on the ALFIW warrants of $3.39 from their $4.57 strike price. So the warrants closed 6 cents above any possible arbitrage scenario. But there were several times during the day when the warrants traded below their intrinsic value. The day high on the stock was $8.56, implying a $3.99 value on the warrants. But the day high on the warrants was only $3.75.

The fact that this has happened twice in three trading days leads us to believe that the funds are slowly losing control on ALF. Continued purchasing of the warrants will eat up the hedge funds inventory and they will be forced or coerced to cover ALF stock to limit their risk exposure. This puts pressure on their finances which will make a short squeeze on the other three stock/warrant combos easier. This impact would likely spread across to other Sabby holdings to some extent, meaning any investor of Sabby owned stocks would be interested in seeing this short squeeze phenomenon spread like wildfire on Sabby's portfolio."

It's one thing for people to spout theories, it's another when they can back up those theories with a recent example of success. We can back up our theories based on what just happened with ALF.

Warrants are like call options that allow warrant holders to buy a company's stock at the strike price. The warrants should therefore follow the stock price less the strike price, or its intrinsic value. Otherwise there is arbitrage. It's easiest just to give an example as illustration. Let's say a stock has warrants with a strike price of $5. The stock spikes to $10 but the warrants trade at only $3. An investor could short sell the stock at $10, buy the warrants at $3 and immediately exercise them for $5. They pay $8 in total to cover their $10 short, pocketing $2 in arbitrage.

Hedge fund shorts know this and will use warrants in this way in order to stimulate arbitrage buyers on the warrants and arbitrage (short) sellers on the stock. The additional shorting puts weakness back on the stock price and allows the hedge fund short to live another day. We saw this very obvious effect on ALF two weeks ago, particularly when it first spiked above $9 on June 16. We saw this carbon copy effect on AUUD and CUEN this past week. Knowing what happened to ALF the following days, we know these games can't last long and shorts will break down and be forced to cover.

AUUDW has a strike price of $4.54. The stock price reached a high of $9.30 on June 29. The warrants were worth $4.76 at the time. However, the day high on the warrants was only $3.79, about $1 below their intrinsic value. Now some of that gap can be explained by illiquidity on the warrants, but most of that is going to be due to the effect of hedge funds trying to get arbitrage players to short the stock and put downward pressure on it, relieving the pressure on their shorts. Thursday's result is even more blatant because of the stock's strong close. At $7.35, the warrants are worth $2.81, but they closed at $2.60. They were consistently $0.50 or more below intrinsic value until the very last few moments of the day when they started moving up. Notice how the stock pulled back from the day high made around 3:40 while the warrants were getting stronger. This, to us, is a sign that the warrants were being purchased and the stock shorted to take care of the arbitrage. The funds desperately tried to put a lid on the stock price in the last few minutes but mostly failed. On Friday AUUDW closed up 10% to $2.87 despite the stock moving up only 1%. It closed the arbitrage gap as its intrinsic value of $2.88 based on the stock's $7.42 close is only one penny off the actual close. But the hedge fund shorts are still obviously hurting.

How do you stop this manipulation? By consistently buying up the warrants so that they don't fall below their intrinsic value and arbitrage players try to short the stock. This also eliminates the inventory of warrants for the funds that are using them as insurance to aggressively short the stock.

CUEN and CUENW also had a very blatant and egregious attempt at this style of shorter manipulation. CUEN had a day high of $9.25 on June 30 and the warrants have a strike price of $4.30. Therefore the warrants had an intrinsic value of $4.95. But they traded at a day high of only $3.86. Throughout the day the warrants were often trading $1 below intrinsic value and the stock was aggressively walked down. Thursday's trading wasn't as egregious but there were still times when the warrants traded below their intrinsic value. The stock's day high was $7.49, implying a $3.19 value on the warrants. But the warrants day high was only $3.05. Finally on Friday things came into check as the stock price closed at $6.45. The warrants closed at $2.43, comfortably above the $2.15 intrinsic value.

Hedge funds shorts have played their hands on AUUD and CUEN and we know that the same problems for them on ALF exist on these two stocks as well. Problems for them mean benefits for retail investor longs who want to support these companies and cause a squeeze against these shorting scumbags.

Obvious question: Why would the funds want to sell the warrants if that's the tool they use as insurance to short the stock?

They wouldn't, not all of them necessarily. But if you read our previous pieces, they might not have a choice in a squeeze situation. The funds don't WANT to sell their warrants, but they will in times of desperation to put a lid on the stock's price. Warrants are sold below their intrinsic value so that investors took advantage of the arbitrage, selling or short selling the shares to try to put selling pressure on the stock price.

CUEN is being heavily shorted today from $7.75 to 5.80 today! WTF. Is WSB on this yet? So many bag-holders diamond-handing this. Please help! CUEN or CUENW need VOLUME to run. Apes Strong Together!

ReplyDeleteI hope you will take another look at GOED. They have been under heavy short attacks the last 2 weeks and pretty much took back the latest pump. Def something weird going on as there has been no news.

ReplyDeleteIn the long run, the hedge funds won. They only are losing in amc and gme. They will just wait it out. Every stock listed in this article two month later is down 50%

ReplyDelete