The ALF-Like Squeeze Has Begun For AUUD And CUEN - Buy The Warrants

Yesterday we compared ALF with AUUD after it broke out on June 15. With AUUD's fourth day of the post-news breakout in the books, the similarities are absolutely uncanny:

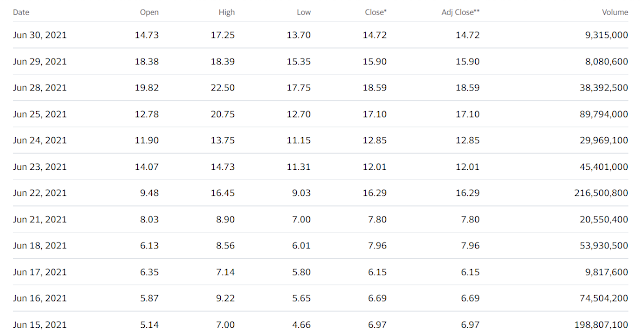

This is ALF's price performance:

June 15 was the first day ALF broke out and closed above $5. June 28 was the first day AUUD broke out above $5. Here are the similarities to these two three-day sets:

1. Both day ones represented a break out on massive volume.

2. While day two had volumes going in opposite directions, day three saw a substantial decline in volume versus the prior two days.

3. Both hit a day high above $9 before pulling back significantly on day two.

4. Both day threes had a gap down from day two's close and finished off about 30 cents from the day low.

5. Both stocks closed day three at a lower price than day one.

Now let's look at day four. AUUD shot up to $7.35 on 9.6 million volume. This is about double of day three's volume but still much less than day one or day two. On ALF's day four, the stock shot up 29% from $6.15 to $7.96. volume was five times higher than day three but less than on day one and day two.

What does this tell us? Just like ALF, AUUD is reversing its "pump and dump" chart and is headed for a second round of highs. When stocks spike on heavy volume on news, then that volume dissipates, the stock price almost always trends down too. Day traders and other flippers are losing interest while the news isn't enough to attract real investors. Shorts then benefit by pounding the stock downwards. Both ALF and AUUD have gone UP on lower volume. ALF closed 14% higher on day four versus day one, $7.96 versus $6.97. AUUD closed 25% higher on day four versus day one, $7.35 versus $5.89. They are going up on less volume. Day traders are leaving as the pump and dump charts on day two and day three suggest, but real investors have taken their place. Shorts have failed to bring the stock down and are now in a poor spot. Doubly poor since they just took a big hit on ALF and GOED.

The other huge tell is on the warrants. This is what we said on ALF on June 20th:

"ALF is up 19% in those three days, and has nearly tripled from its May 4 close of $2.90. Its trading has been very solid since it announced the installation of 10,000 digital screens in Uber and Lyft vehicles in Miami on the 15th. While many stocks in similar situations exhibit a "pump and dump" chart and sell off days after the news, ALF has had bullish action since then. The shorts and hedge funds tried bringing it down with weak opens on June 16 and June 17. But it has failed. We mentioned above about how the warrants traded below their intrinsic value last Wednesday when it blasted off to over $9. It happened again on Friday. The $7.96 close on the stock implies an intrinsic value on the ALFIW warrants of $3.39 from their $4.57 strike price. So the warrants closed 6 cents above any possible arbitrage scenario. But there were several times during the day when the warrants traded below their intrinsic value. The day high on the stock was $8.56, implying a $3.99 value on the warrants. But the day high on the warrants was only $3.75.

The fact that this has happened twice in three trading days leads us to believe that the funds are slowly losing control on ALF. Continued purchasing of the warrants will eat up the hedge funds inventory and they will be forced or coerced to cover ALF stock to limit their risk exposure. This puts pressure on their finances which will make a short squeeze on the other three stock/warrant combos easier. This impact would likely spread across to other Sabby holdings to some extent, meaning any investor of Sabby owned stocks would be interested in seeing this short squeeze phenomenon spread like wildfire on Sabby's portfolio."

It's one thing for people to spout theories, it's another when they can back up those theories with a recent example of success. We can back up our theories based on what just happened with ALF. The other key to understanding AUUD's imminent squeeze is in the warrants.

Warrants are like call options that allow warrant holders to buy a company's stock at the strike price. The warrants should therefore follow the stock price less the strike price, or its intrinsic value. Otherwise there is arbitrage. It's easiest just to give an example as illustration. Let's say a stock has warrants with a strike price of $5. The stock spikes to $10 but the warrants trade at only $3. An investor could short sell the stock at $10, buy the warrants at $3 and immediately exercise them for $5. They pay $8 in total to cover their $10 short, pocketing $2 in arbitrage.

Hedge fund shorts know this and will use warrants in this way in order to stimulate arbitrage buyers on the warrants and arbitrage (short) sellers on the stock. The additional shorting puts weakness back on the stock price and allows the hedge fund short to live another day. We saw this very obvious effect on ALF two weeks ago, particularly when it first spiked above $9 on June 16. We saw this carbon copy effect on AUUD on Tuesday and again today. Knowing what happened to ALF the following days, we know these games can't last long and shorts will break down and be forced to cover.

AUUDW has a strike price of $4.54. The stock price reached a high of $9.30 on June 29. The warrants were worth $4.76 at the time. However, the day high on the warrants was only $3.79, about $1 below their intrinsic value. Now some of that gap can be explained by illiquidity on the warrants, but most of that is going to be due to the effect of hedge funds trying to get arbitrage players to short the stock and put downward pressure on it, relieving the pressure on their shorts. Thursday's result is even more blatant because of the stock's strong close. At $7.35, the warrants are worth $2.81, but they closed at $2.60. They were consistently $0.50 or more below intrinsic value until the very last few moments of the day when they started moving up. Notice how the stock pulled back from the day high made around 3:40 while the warrants were getting stronger. This, to us, is a sign that the warrants were being purchased and the stock shorted to take care of the arbitrage. The funds desperately tried to put a lid on the stock price in the last few minutes but mostly failed.

How do you stop this manipulation? By consistently buying up the warrants so that they don't fall below their intrinsic value and arbitrage players try to short the stock. This also eliminates the inventory of warrants for the funds that are using them as insurance to aggressively short the stock.

As discussed yesterday, CUEN and CUENW had very blatant and egregious attempt at this style of shorter manipulation. CUEN had a day high of $9.25 and the warrants have a strike price of $4.30. Therefore the warrants had an intrinsic value of $4.95. But they traded at a day high of only $3.86. Throughout the day the warrants were often trading $1 below intrinsic value and the stock was aggressively walked down. Today's trading wasn't as egregious but there were still times when the warrants traded below their intrinsic value. The stock's day high was $7.49, implying a $3.19 value on the warrants. But they warrants day high was only $3.05.

Hedge funds shorts have played their hands on AUUD and CUEN and we know that the same problems for them on ALF exist on these two stocks as well. Problems for them mean benefits for retail investor longs who want to support these companies and cause a squeeze against these shorting scumbags.

Obvious question: Why would the funds want to sell the warrants if that's the tool they use as insurance to short the stock?

They wouldn't, not all of them necessarily. But if you read our previous pieces, they might not have a choice in a squeeze situation. The funds don't WANT to sell their warrants, but they will in times of desperation to put a lid on the stock's price. Warrants are sold below their intrinsic value so that investors took advantage of the arbitrage, selling or short selling the shares to try to put selling pressure on the stock price.

This is great! Spot on so far. Please post an update after fridays market just gone

ReplyDelete