They say to never trust an anonymous blogger on the internet. And I am an anonymous blogger. I have my reasons for remaining anonymous, and those reasons don't matter. Can you really trust articles on Bloomberg or Wall Street Journal any more than an anonymous opinion? All I ask is to debate the content of my message. Not who I am or my motivations. If you agree with what I say and think that it's in-depth, quality and truthful work, then make sure to share this on every retail channel available to you. Reddit, Discord, Stocktwits, Twitter, Telegram, Whatsapp, Tiktok and wherever else. I have just added a follow option at the top left for those who want to be notified when more blogs come out.

Last Wednesday evening I talked about the gamma squeeze potential of Gores Guggenheim, Inc. (GGPI) a.k.a. the "Polestar SPAC" and Cassava Sciences, Inc. (SAVA). SAVA worked out pretty well as when it crossed and stayed above the $50 mark, that forced the funds to buy the stock in order to protect against exposure to in-the-money calls. That $6 move in two days was enough to collect decent call option profits.

GGPI didn't work out as it was taken down by the EV sector pullback. LCID, RIVN, SEV and FSR all dropped heavily on Thursday before recovering on Friday, a trend that GGPI was caught up in. That's okay though, because GGPI looks as strong as ever both from a fundamental and technical perspective.

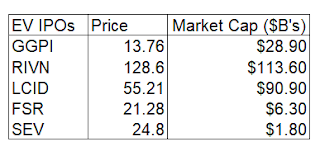

A blog post on Seeking Alpha with a target of $35 put forth a straightforward fundamental argument for going long GGPI. Polestar sold and delivered 10,000 EV cars so far in 2020 with expectations to deliver 29,000 on the year. This compares very well to RIVN, FSR and LCID which have delivered only a handful of vehicles and have very little revenue at this time. Despite Polestar being far ahead of these other recent EV IPOs, its market cap sits at just a fraction of RIVN and LCID. Here is an update as of Friday's close:

GGPI's market cap estimate is based on proposed post-merger shares of approximately 2.1 billion. That leads to a $29 billion market cap which is about three times lower than RIVN and LCID. The Seeking Alpha article's target of $35 would imply a market cap of $74 billion. A $50 stock price would imply a $105 billion market cap. This would place GGPI comfortably between RIVN's and LCID's valuation while being far ahead of both of them in terms of deliveries and revenues. Polestar has a chance to be the #2 EV manufacturer behind Tesla. That could justify a stock price well above $50 in the long run. but first thing is first, there is a lot of profits to be made by holding out for $50 or $35.

For those bears who think RIVN and LCID should collapse, even if they dropped by half, you could still justify GGPI nearly doubling to $25 just to come in line with those two companies reduced market caps.

There are two factors in addition to the favorable industry comparison fundamentals that present a strong bullish case on GGPI. First, it will only be natural for the stock price to rise on hype as the date of the merger taking place nears. That's expected to occur in early 2022. Polestar has had a steady stream of news while continued news of the merger's imminent occurrence will add to the buying pressure.

The other factor will be the gamma squeeze potential because of the high demand for call options. This is a screen shot of call options outstanding for December and January.

Even though November calls were in the focus for the final day, both of these sets of calls achieved some decent volume. Especially the ones at $15. But the open interest is something to pay special attention to. Two weeks ago, the $10 calls were slightly in the money with the strike prices at $12.50 and above out of the money. Now the $10 calls are deep in the money, the $12.50's are in the money and the $15's are challenging that status.

There are a combined 43,832 call option contracts open at the $10 and $12.50 strikes for December and 75,153 for January. Adding in the small amount of open interest at $7.50 strikes and below, if the funds that are writing these contracts are trying to remain delta neutral, this is over 12 million shares locked up in call option contracts that are reasonably expected to expire in the money over the next two months. That's a massive amount of the 80 million pre-merger shares outstanding on GGPI.

Now come the $15 calls. There are 32,748 call options open between the December and January expiries. That represents an additional 3.3 million in shares that are to be purchased and locked up in an attempt to be delta neutral should those calls go from being OTM to ITM as GGPI surpasses $15. Keeping in mind that November expiry was last Friday, the focus of trading would have been on those calls. Yet the December $15 calls experienced 8,711 of volume on that day and 2,038 for January. That type of buying is only going to increase as the interest in the stock and the December expiry date nears. Some of that volume will be from flippers and those who closed off their previously opened positions, but my guess is that this volume will add significantly to the open interest (daily volume calculations on open interest net changes are recorded in the next trading day's open interest).

Having a look at the strikes at $17.50 and above, there are 49,701 open calls for December and 36,257 open calls for January. That's an additional 8.6 million in shares that get locked up in delta neutral call option positions by the option writers should these go in the money.

Keep in mind that this is a snapshot of the numbers TODAY. These numbers are only going to increase based on the high level of interest of call options already and increases in speculation. Below is a summary of a chart assessing the gamma squeeze potential.

Once the merger takes place, Polestar will have over 2 billion shares outstanding. This is a consideration for long term valuation (keeping in mind we already know it's way undervalued versus LCID and RIVN), but for near term squeeze potential, all we care about is the current number of GGPI shares outstanding. Out of 80 million shares, already over 16 million of them are allocated for delta neutral in-the-money call option hedges for all expiries between December and 2024. If we consider the OTM calls expiring over the next two months, there's a potential nearly 30 million of shares locked in call option hedging strategies.

GGPI is a benefactor of having a very big story packed into a relatively small float into the SPAC. Current GGPI holders will be diluted by 20 times, as they should. Polestar is bringing A LOT to the table. Eventually that float is going to grow to 2 billion post-merger. However, GGPI is receiving a disproportionate amount of interest in call options RIGHT NOW because of this story.

What I'm trying to say is that in a normal IPO world, Polestar would have over 2 billion shares outstanding and the call option open interest that's generating 10's of millions of shares potentially locked in hedging strategies would not be a major factor to create a gamma squeeze. However, on a float of 80 million this IS a major factor.

Let's put it into perspective. BKKT is a recent SPAC merger that generated a lot of investor interest. ICE owns approximately 175 million of the 250 million shares, but those shares are locked for several months. So in effect, BKKT has 50 million shares outstanding right now with the balance of non-ICE held shares expected from the PIPE share unlock happening soon. The stock recently ran from $10 to as high as $50 on retail interest and high option demand that placed it into temporary gamma squeeze-like territory. That was on a stock that had 50 million shares accessible to the market when in reality it has 250 million shares. Think about that impact on a stock like GGPI, which currently has 80 million shares outstanding but in reality with have over 2 billion shares once the Polestar merger completes.

Comments

Post a Comment