The Top 5 Short and Gamma Squeeze Candidates Heading Into Next Week - TRUP, KRYS, GEVO, ABUS, GGPI

I created this blog as there is too much censorship on the Wallstreetbets Reddit forum now and it's bought and paid for by the institutions. They say to never trust an anonymous blogger on the internet. And I am an anonymous blogger. I have my reasons for remaining anonymous, and those reasons don't matter. Can you really trust articles on Bloomberg or Wall Street Journal any more than an anonymous opinion? All I ask is to debate the content of my message. Not who I am or my motivations. If you agree with what I say and think that it's in-depth, quality and truthful work, then make sure to share this on every retail channel available to you. Reddit, Discord, Stocktwits, Twitter, Telegram, Whatsapp, Tiktok and wherever else. I have just added a follow option at the top left for those who want to be notified when more blogs come out.

These are the top five shorts and gamma squeeze candidates heading into next week's monthly option expiry. All of these stocks either have a heavy short squeeze potential, high open interest and volume on near term call options or are undeniably fundamentally undervalued. Or all of these things. I start with the best short squeeze catalysts and end with the best fundamental plays. These five stocks are Trupanion, Inc. (TRUP), Krystal Biotech, Inc. (KRYS), Gevo, Inc. (GEVO), Arbutus Biopharma Corporation (ABUS) and Gores Guggenheim, Inc. (GGPI). In the interest of making this as short as possible, I will be linking back to previous writeups that explain the background of my reasoning. This is applicable on all of these stocks except GEVO, which is my first time writing about it.

#1 Trupanion, Inc. (TRUP)

Background reading: https://wallstreetbetsreddit.blogspot.com/2021/12/trupanion-is-new-gamestop-partners-with_7.html

This is the top short squeeze candidate. TRUP announced that it's teaming up with Chewy, Inc. (CHWY) to offer pet insurance to Chewy's base. If you recall, CHWY founder Ryan Cohen was the one who joined GameStop (GME) to initiate a turnaround plan, causing the famous short squeeze to over $400. This news caused the stock to blast off 39% on Tuesday while the stock settled at $152.20 today.

TRUP has about about 4 million shares short on a float of 31 million shares and total shares outstanding of 40 million. So it doesn't have as high of a short interest as other stocks known for their short squeeze potential. Though TRUP's short interest % of float of about 13% is comparable to GME's today. What makes TRUP such a strong short squeeze candidate becomes apparent when looking at the NASDAQ short interest history. Short interest has been steadily rising since the stock was around $80 in April. When it pulled back to that mark in September, shorts should have been smart and covered. But instead they shorted even more. The key here is the days to cover. The short interest of 4 million shares is 10 times greater than the daily average volume. Most of those shorts are losing something close to 100% while the stock is over $150.

Looking at Ortex data, not a lot of the short interest has covered. 3.7 million shares are borrowed and there is likely naked short positions as well. Yesterday saw a net 65,000 shares covered while today saw a net 11,000 more shorted. These numbers are insignificant when compared to the short interest. I believe that this is a sign that shorts are in major trouble. If they could short more, they would at over $150. But the fact that they are holding instead of adding to their position tells us that they are near a margin call or some other sort of risk mitigation factor. They also haven't covered yet in hopes that the stock will cool off and they can cover at a lower price.

Here is the problem for them. There are 4 million shorts outstanding. Yesterday's volume was 2.6 million and that moved the stock up $43. Today's volume is 870,000. Daily volume is usually 350,000. Volume is slipping quickly and if the stock remains this high, a margin call on one short can create enough buying pressure to raise the price substantially and cause a domino effect on the other shorts, creating that major squeeze.

When AMC traders point to Volkswagen's (VWAGY) massive short squeeze in 2008, it happened on a stock that trades very little volume, not one that trades tens of millions of shares in a day. TRUP is a much closer comparable to a stock like Volkswagen.

TRUP's options don't have a lot of open interest so there's not much of a chance of a gamma squeeze being the main driver. Though the $195 strike December calls (the highest strike available) are getting the most action.

#2 Krystal Biotech, Inc. (KRYS)

Background reading: https://wallstreetbetsreddit.blogspot.com/2021/11/gamma-squeeze-and-covid-variant-top.html

KRYS is the second best short squeeze candidate, and shares some characteristics similar to TRUP while some are different. KRYS recently closed a $75 offering. This provided shorts a temporary reprieve after the stock spiked over $90 last week and they are definitely taking advantage of it. The Ortex data shows that borrowed shares are at 560,000, down from 760,000 from a week ago. The short interest was over 2 million as of 11/15, so shorts are definitely licking their wounds and covering. This also shows why TRUP shorts aren't covering yet and what they hope will happen. Just like on KRYS, they had big losses as the stock shot up. They hope the stock will pull back a bit before covering. If it doesn't happen, they will be forced to cover at high prices. Unlike KRYS, TRUP isn't a biotech in need of a high amount of cash so an offering is very unlikely to come to provide shorts that reprieve.

KRYS, just like TRUP, daily volume is quickly declining. KRYS was up 7% today to $76.20 on only 730,000 volume. The remaining shorts outstanding plus any naked shorts would do well to cover while they can. KRYS could easily spike back to the $100 range now that the offering is closed. KRYS has only 25 million shares outstanding and a 16 million float.

KRYS has a much more robust options market than TRUP. Before the breakthrough news, KRYS was trading under $40. Now every call option from $40 to $75 has just gone from out-of-the-money to deeply in-the-money. That's a total of 13,820 call options for the December expiry alone. The $70 strike calls saw 2,800 in volume today. We will see tomorrow if that was a closing of a profitable position or the opening of additional open interest. The call options at these strikes represent 1.4 million shares or 9% of the float potentially locked up in delta neutral hedging strategies from funds that write the calls.

There are an additional 5,272 December call options open at the $80 to $100 strikes. Should the stock continue to rise, the gamma squeeze potential increases as more of these turn in-the-money and more people bet on options as the stock rises heading into next week's expiry date. These options would represent another 527,000 of shares potentially locked up in delta neutral hedging strategies from call option writers.

#3 Gevo, Inc. (GEVO)

This is where we start to balance out short squeeze potential with fundamentally undervalued opportunities. GEVO signed its largest renewable fuels supply contract to-date yesterday, an eight year deal with Kolmar for $2.4 billion. Despite that, the stock only moved up $0.40 on December 7th from $5.15 to $5.55, while adding another $0.10 today. This is only an additional $100 million in market cap for the largest deal signed in company history - one-third of the amount of revenue expected, $300 million, in the first year of the deal alone. The market is clearly undervaluing this news, and it's pretty obvious that shorts are having a role in keeping the price down.

Ortex data shows 48 million shares are on loan, up from 44 million a week ago. This is about 25% of the float and also means four million additional shares were shorted this past week. Today alone saw an additional 870,000 borrowed. The increase in short interest coincides with a $500 million at-the-market offering announced in September. Though the company is limited as to how many shares it can issue as it has 250 million authorized shares. There will be a vote to increase the authorized total to 500 million in January, but it remains to be seen if that will be successful. GEVO had $500 million in cash and equivalents as of September 30, so the company is in no rush to dilute. Though the shorts are certainly betting on it.

I think this is a case of shorts getting aggressive and greedy. This would be a good stock to short in a weak market. However, the market is proving to be more resilient than expected with the Fed tapering and Omicron variant news. Watch for a wave of covering. A month ago GEVO was around $7.50. I think based on this news it's deserving to return to at least to that level.

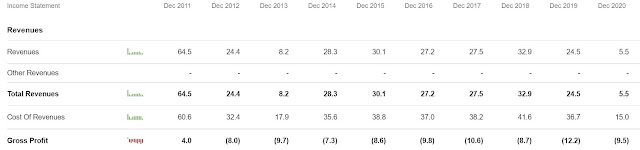

There was a suspiciously timed article called Don't Buy GEVO Stock that in essence said that the stock will never be profitable and is nothing more than a science experiment. It's true that GEVO didn't achieve gross profit since 2011. But the author only tells part of the story. GEVO had $65 million in revenue that year and $4 million in gross profit. At no other time did the company come close to that level of revenue. It's not much of a stretch to believe that if the company can surpass that level of revenue, it would achieve enough scale to once again be operating at a gross profit. The contract with Kolmar is five times this number annually and doesn't account for other business.

#4 Arbutus Biopharma Corporation (ABUS)

Background reading: https://wallstreetbetsreddit.blogspot.com/2021/12/moderna-versus-arbutus-roivants-move-up.html

The case for ABUS is really simple. Last week, there was huge news of the legal decision on the status of a patent owned by Arbutus Biopharma Corporation (ABUS) and its status as an essential component of Moderna, Inc. (MRNA)'s mRNA technology built into its pipeline, namely the COVID-19 vaccine. ABUS initially spiked but has pared back most of those gains.

The market has badly misunderstood the value proposition here and went from too enthusiastic on ABUS to swinging to the opposite end where ABUS is unambiguously undervalued. Although ABUS owns the patents, these patents have been licensed out to a private company called Genevant. So if Moderna was to buy out a company to make this problem go away, Genevant would be the target. Genevant is 16% owned by ABUS and 83% owned by Roivant Sciences Ltd. (ROIV). ROIV also owns 29% of ABUS. However, that's not the only part of it. ABUS also has a license deal that entitles it to single digit royalties on future sales of Genevant products covered by the licensed patents. It would also get 20% of any of Genevant's sales in sub-license deals. Assuming Moderna purchases Genevant, it would still be liable to pay out a royalty to ABUS. Assuming this is 5%, the end result would be an approximate effective ownership split of 80% for Genevant and 20% for Arbutus. Roivant might own 83%, but 5% of its 83% belongs to ABUS. While ABUS would gain another 4% - one point is cannibalized in its existing 16% ownership.

The market is correctly pushing up ROIV's valuation as it is the one that holds the majority stake in Genevant. While ABUS has been up and down, but mostly down, ROIV has made steady gains every day. I believe that this is the market's true valuation of the Genevant patent news. ROIV is much less susceptible to noise from day trading and manipulative shorts. ROIV's moves have been so consistent that the market could no longer ignore it and actually pushed ABUS up 5% to $4.14, its highest close in three days as shorts worked hard to keep it under $4.00.

ROIV may own a larger stake in Genevant, but ABUS is a much smaller company. Therefore ABUS should move significantly more than ROIV because Genevant makes up a higher portion of its overall value. The following chart summarizes the opportunity:

ABUS has increased $0.94 from 11/30 to 12/8, representing a $127 increase in market cap since the MRNA patent news dropped. ROIV, in contrast, has increased from $6.63 to $9.96, adding $2,280 million in market cap. If we sum these two figures together, ROIV has taken 95% of the gain since the news of this deal while ABUS has taken only 5%. When we compare that to the percentage ownership of Genevant, we see these numbers are heavily undervaluing ABUS. This assumes that all of the recent increase in market cap is attributed to the Genevant/MRNA patent news. I think it's fair to say so given that ROIV hasn't had any other news of note and has been a steady rock this past week, one of the few in this volatile market.

There is a slight complicating factor in that ROIV owns 29% of ABUS, but that can be corrected for the most part pretty easily in the following chart:

ROIV increased $2,280 million in market cap since the patent news broke. After adjusting for its stake in ABUS and considering its 80% stake in Genevant, we can assume that Genevant has increased $2.8 billion in valuation over the past week. ABUS is entitled to 20% of this, or $561 million but has increased only $127 million. The end result is that when ROIV is $9.96, a fair price for ABUS should be $7.35. Under this scenario, more adjustments would have to be made as 29% of that gain on ABUS should flow back to ROIV and reduce the Genevant valuation slightly, but I think that people get it that ABUS should definitely be worth far more than $4.14. It's flippers and shorts at fault.

Ortex data shows an increase in shares on loan from 2.7 million to 6.1 million in the past week. ABUS float is pretty big so this still only represents 6.5% of the float. But still, this is the reason why the stock is badly lagging ROIV in its true valuation. Shorts have an interest in manipulating it. 781,000 shares were borrowed while 729,000 were returned. This increased the short position by 52,000 but really shows that it's mainly shorts flipping in and out of positions. The good news is as volume tightens and ROIV keeps rising, this will put pressure on the shorts to cover.

ABUS option data also shows significant open interest. Between the $4 and $5 strikes expiring in December, there is over 23,000 in open interest, representing another potential 2.3 million shares that could be locked up in delta neutral hedging strategies.

#5 Gores Guggenheim, Inc. (GGPI)

Background reading: https://wallstreetbetsreddit.blogspot.com/2021/11/ggpi-gamma-squeeze-potential-increases.html

I end with the one that could be the most fundamentally undervalued. Unfortunately GGPI got taken down pretty badly during the past week as general market volatility hit the electric vehicle sector hard. However, Tesla (TSLA) and Rivian (RIVN) are coming back strong and I think that will flow down to GGPI. GGPI will be merging with Polestar, arguably the #2 electric vehicle producer in the West behind Tesla. GGPI is miles ahead of the other recent EV listings. A blog post on Seeking Alpha with a target of $35 put forth a straightforward fundamental argument for going long GGPI. Polestar sold and delivered 10,000 EV cars so far in 2020 with expectations to deliver 29,000 on the year. This compares very well to RIVN, FSR and LCID which have delivered only a handful of vehicles and have very little revenue at this time. Despite Polestar being far ahead of these other recent EV IPOs, its market cap sits at just a fraction of RIVN and LCID. There was also a post on Wallstreetbets with in depth analysis and I recommend reading it as well.

I took the opportunity to load up on GGPI April $10 calls on this pullback. The merger with Polestar is expected to take place in Q1. The $10 April calls are trading about $0.50 less than the GGPIW warrants. So I sold those warrants to buy the calls. The warrants may have a 5 years time to expiry, but warrants tend to trade below their intrinsic value when a SPAC stock runs a lot. Just compare DWAC to DWACW as an example. The warrants also have a strike price of $11.50 versus the options at $10, so that is a free $1.50 I was willing to trade for the additional time to expiry which I don't think I will need.

Ortex data shows 5.2 million shares are out on loan. This is down from 7.6 million from a week ago, but up from 3.1 million in short interest as of 11/15. I have talked at length about the gamma squeeze potential and open interest analysis on call options. Short interest in conjunction with large call option open interest is conducive to gamma squeezes and it looks like GGPI is in better position than ever before for it. But GGPI exists mostly as a fundamental value play. A cheaper alternative to Rivian or Lucid while ahead of the game on both of those companies in terms of EV production.

Disclosure: I am long TRUP, KRYS, GEVO, ABUS, GGPI call options and/or stock.

I don't think GEVO can be squeezed. This might be the companies expecting to buy in after the share increase is approved. If you expect to buy 100 million shares you could easily short 50 million to keep the price down. It would require a huge amount of buyers to stop this manipulation.

ReplyDeleteI dont see anything here re: APYP

ReplyDelete