Think of Arbutus as AMC and Moderna as Citadel. Take ABUS to $1,000 and Make Moderna Pay!

I created this blog as there is too much censorship on the Wallstreetbets Reddit forum now and it's bought and paid for by the institutions. They say to never trust an anonymous blogger on the internet. And I am an anonymous blogger. I have my reasons for remaining anonymous, and those reasons don't matter. Can you really trust articles on Bloomberg or Wall Street Journal any more than an anonymous opinion? All I ask is to debate the content of my message. Not who I am or my motivations. If you agree with what I say and think that it's in-depth, quality and truthful work, then make sure to share this on every retail channel available to you. Reddit, Discord, Stocktwits, Twitter, Telegram, Whatsapp, Tiktok and wherever else. I have just added a follow option at the top left for those who want to be notified when more blogs come out.

Today's blog will be about the huge news of the legal decision on the status of a patent owned by Arbutus Biopharma Corporation (ABUS) and its status as an essential component of Moderna, Inc. (MRNA)'s mRNA technology built into its pipeline, namely the COVID-19 vaccine. This is very well known news today so I won't get into the details of the legal issue, but there are several misconceptions with who owns what and some disconnects with the math.

First, although ABUS owns the patents, these patents have been licensed out to a private company called Genevant. So if Moderna was to buy out a company to make this problem go away, Genevant would be the target. Genvant is 16% owned by ABUS and 83% owned by Roivant Sciences Ltd. (ROIV). ROIV also owns 29% of ABUS. However, that's not the only part of it. ABUS also has a license deal that entitles it to single digit royalties on future sales of Genevant products covered by the licensed patents. It would also get 20% of any of Genevant's sales in sub-license deals. Assuming Moderna purchases Genevant, it would still be liable to pay out a royalty to ABUS. Assuming this is 5%, the end result would be an approximate effective ownership split of 80% for Genevant and 20% for Arbutus.

ROIV may own a larger stake in Genevant, but ABUS is a much smaller company. Therefore ABUS should move significantly more than ROIV because Genevant makes up a great portion of its value. The stock prices of ABUS and ROIV were all over the place today. ABUS moved first then pulled back and ROIV shot up later in the day. But an analysis of the stock price movements shows something is clearly off:

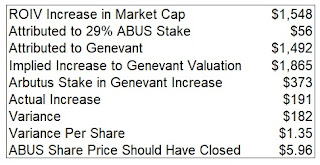

ROIV increased $1.548 million in market cap but ABUS increased only $191 million. Despite having a 20% interest in Genevant, it only received 11% of the associated market cap increase, if one assumes 100% of both companies' increase in market cap can be attributed to the patent news. This calculation is further complicated by ROIV's 29% stake in ABUS, but that can be corrected relatively easily:

ROIV increased $1,548 million. 29% of ABUS' increase of $191 million belongs to ROIV, but that is only $56 million, leaving $1,492 attributed to Genevant. Assuming an 80/20 split, this should have resulted in $1,865 million increase to Genevant's valuation, leaving $373 million for ABUS. The end result was that ABUS should have moved an additional $182 million in market cap and closed at $5.96. Now I know that the $182 million would result in another 29% belonging to Genevant - $53 million - but that would force me to make adjustments back and forth forever to get these numbers dead on. Let's just say that with no ambiguity, ABUS is underpriced relative to ROIV.

Let's get to the heart of the matter. Is a $2 billion valuation nearly enough? MRNA dropped $14 billion in market cap today, though a lot of that could be attributed to the market - although PFE was green today. Buying out Genevant not only gets rid of Moderna's legal issues, it brings up potential patent disputes over the use of mRNA tech, including the one in the BNTX/PFE vaccine. MRNA could push for legal action on BNTX if it bought out Genevant.

Let's say a final deal is for $5 billion. Assuming 20% of that belongs to ABUS, that's $1 billion right there. That would justify a $10 stock price. $1 billion for Genevant plus $350 million in value for ABUS' other initiatives. But let's say instead it's $10 billion. $2 billion of that would belong to ABUS and by then we are talking about a stock price heading towards $20.

This legal loss looks particularly bad on Moderna, which refuses to share its vaccine formula to developing countries so that they can vaccinate their population. It would be best to make this issue go away as soon as possible.

Now that we have the numbers out, and they look good for ABUS, we can talk about the meme status of the stock. There are only 2.4 million shares short, a pretty low 2% of the float considering that this is a biotech. Shorts have been wisely avoiding shorting ABUS as they likely know the value and risk of doing so given the patent case. However, there is another way of getting a gamma squeeze.

Call option volume was intense. Over 90,000 December expiry calls traded today, though we will have to wait until tomorrow to see how many carried to open interest. If a substantial amount of them do, that could result in millions of shares being locked up in delta neutral hedging strategies by the funds as the write calls and buy the stock as insurance.

If investors get this stock moving, ABUS will stay in the limelight and this embarrassing situation for MRNA will not go away until they do something about it. Continue to buy up ABUS and make MRNA pay!

Disclosure: I am long ABUS

great information!! Thanks

ReplyDeleteSorry, no offense. You said take ABUS to $1,000 yet you're talking a deal of $5B and ABUS gets $1B (136M OS shares) ends up $7.35 pps for ABUS which a big gap between $1,000 pps.

ReplyDeleteI'm red everyday but following you lol.

ReplyDelete